Asian Impact Management Review is an affiliate of Asian Institute for Impact Measurement and Management

Magazine

How Taxonomy of Sustainable Finance and Environmental Impact Assessment May Contribute to Impact Measurement and Management?

Summary: Environmental issues typically involve various objective scientific studies. Practitioners may need to recognize the importance of science-based governance and embrace the core principles of pursuing human health and well-being when conducting environmental impact assessment.

National Academy Press (1999) indicated that the primary goals of a transition toward sustainability over the next two generations should be to meet the needs of a much larger but stabilizing human population, to sustain the life support systems of the planet, and to substantially reduce hunger and poverty. This concept affirms the importance of economic development and human well-being as the ultimate purpose of the environmental impact measurement for all kinds of project activities and its impact assessments. For environmental sustainability, the time horizon matters. In a short period of time, almost any development appears sustainable. In large-scale and long-term dimensions of the future, the carbon cycle and climate change will impact life support systems and human well-being.

Basic Concepts of Sustainable Finance Principles

According to the Principles for Responsible Banking (PRB) published by United Nations Environment Programme (UNEP), a financial institution is expected to align its business strategy to be consistent with and to contribute to individuals’ needs and society’s goals, as expressed in the Sustainable Development Goals (SDGs), the Paris Climate Agreement, and relevant national and regional frameworks. Then the institution will continuously increase its positive impacts while reducing the negative impacts on and managing the risks to people and the environment resulting from its activities, products, and services. These two fundamental principles – alignment with the SDGs and creating positive impacts (or reducing the negative impacts) – almost apply to every sustainable finance standard.

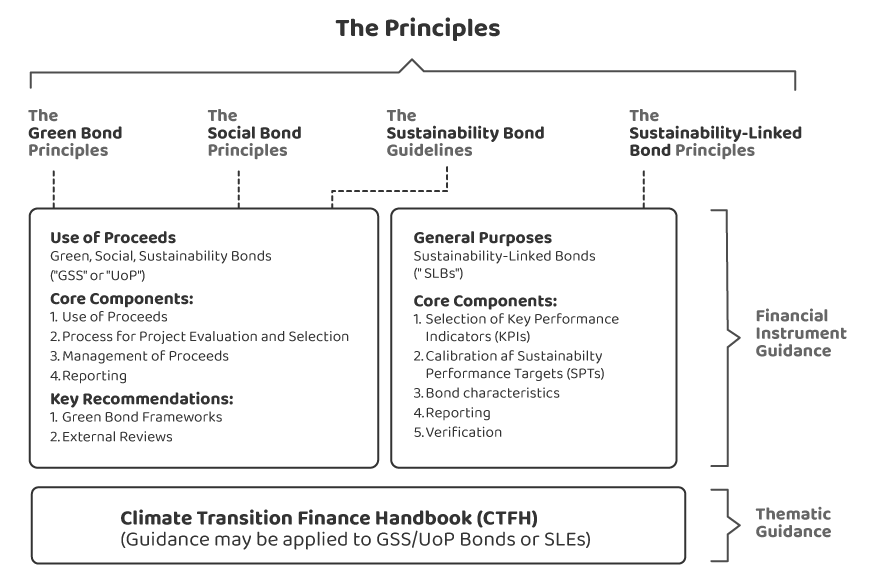

For example, the Green Bond Principles (GBP) published by International Capital Market Association (ICMA) is one of the most prevailing green bond standards in the capital market. GBP requires the issuer to prepare public disclosure report upon four core components, including the process for Project Evaluation and Selection and the Reporting (on its project impacts) as shown in Figure 1:

Source: ICMA (2021)

The concept of the four core components requires bond issuers to develop an investment plan that includes its documentation, such as the environmental benefit guidelines for investment project selection, the establishment of project codes and application forms, as well as internal procedures and methods for collecting related Key Performance Indicators (KPIs), and also the planning and selection of feasible projects for implementation. Issuers of sustainability, green or social bonds must not only comply with the Taipei Exchange Operational Directions for Sustainable Bonds but also align project benefits with the SGDs. Moreover, considering the taxonomy developed by major economies, it ensures that the project’s environmental benefits are significant enough to demonstrate sufficient ambition in achieving the Paris Agreement or local sustainable development goals. A stringent taxonomy often incorporates the Do No Significant Harm (DNSH) principle, ensuring that while a project achieves positive environmental impacts, it does not cause significant harm to important aspects ultimately relating to human health and well-being.

Positive Contribution: Understanding Green Finance

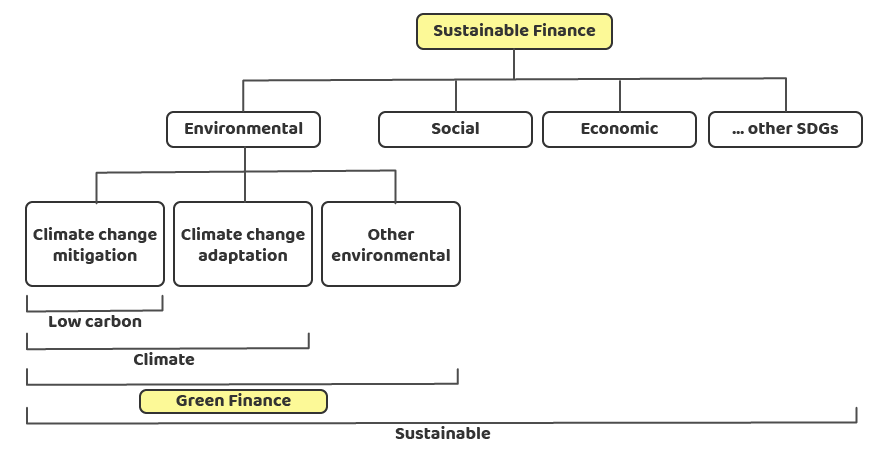

In sustainable finance standards, aligning with international sustainability goals, particularly the United Nations Framework Convention on Climate Change (UNFCCC), means that project objectives are consistent with the Paris Agreement goals, which aims to limit a global average temperature rise of 1.5 degrees Celsius since the Industrial Revolution. However, within the realm of green finance, it is not solely focused on greenhouse gas reduction. Referring to the definition of sustainable finance by the UNEP (Forstater & Zhang, 2016), the classification of sustainable finance, as shown in Figure 2, includes climate change mitigation, climate change adaptation, and other environmental benefits.

Source: UNEP (2016)

Therefore, in recent years, environmental impact assessments have garnered considerable attention, particularly in assessing whether a project can ensure that its related funding is used to achieve a net-zero solution within a scientifically-grounded framework aligned with the Paris Agreement goals. As a result, the target-setting methodology of the Science Based Targets initiative (SBTi) has been widely referenced and scrutinized. However, even if a project does not fully meet the science-based targets of the Paris Agreement goals, it can still generate a positive environmental impact and adhere to the principles of Measurement, Reporting and Verification mechanisms to assess the effectiveness of climate change mitigation and greenhouse gas reduction. It’s worth noting that projects that are not proactive enough cannot claim to be eligible green projects according to rigorous taxonomy.

Negative Impact: Environmental Impact Assessment and Mechanisms

Taking the current Environmental Impact Assessment (EIA) in Taiwan as an example, the Environmental Impact Assessment Act and the Operational Regulations for Environmental Impact Assessment of Development Activities are crucial references for actual operations. The guidelines require assessed development projects to address the following aspects: (1) physical and chemical factors (meteorology, air quality, noise and vibration, odor, hydrology and water quality, soil, geology and topography, waste; (2) ecology; (3) landscape and recreation; (4) socio-economic factors; (5) transportation; (6) culture; and (7) environmental health. The investigation items are adjusted by referring to environmental regulations, relevant standards, environmental indicators, and monitoring information networks.

With the Technical Specification for Health Risk Assessment as an example, the steps of environmental impact assessments include hazard identification, dose-response assessment, exposure assessment, and risk characterization. Based on the results of the first three steps, estimates are made to calculate the total carcinogenic and non-carcinogenic risks of residents exposed to various hazardous chemicals within the scope of the development activity. The total non-carcinogenic risk should not exceed a hazard index (HI) of 1. Suppose the total carcinogenic risk exceeds 10-6; in that case, the development entity must propose the best feasible risk management strategy and undergo review by the Environmental Impact Assessment Review Committee of the Environmental Protection Agency. Risk estimation should involve uncertainty analysis, with the 95% upper limit value as the criterion.

Environmental impact management involves various objective scientific studies and necessitates the identification of at least one positive contribution. The extended concept of DNSH also encompasses the essence of human rights and biodiversity. When discussing environmental impact management, we need to recognize the importance of science-based governance and embrace the core principles of pursuing human health and well-being as well as sustainable development.

Reference

- Forstater, M., & Zhang, N. (2016). Definitions and concepts: Background note. UNEP Inquiry: Nairobi, Kenya.

- International Capital Market Association. (2021). Green Bond Principles—Voluntary Process Guidelines for Issuing Green Bonds—June 2021.

- National Research Council. (1999). Our common journey: a transition toward sustainability. National Academies Press.

- UNEP Finance Initiative. (2021). Responsible Banking: Building Foundations. The first collective progress report of the UN Principles for Responsible Banking signatories.

To cite this article, please use:

Tseng, R. (2023). How taxonomy of Sustainable Finance and Environmental Impact Assessment may contribute to Impact Measurement and Management? Asian Impact Management Review, Volume 2 (1), Summer 2023. http://doi.org/10.30186/AIMR.202307.0001

About the Author

Roger Tseng

Roger Tseng is the Partner of Climate Change, Sustainability Services and ESG Advisory at Ernst & Young. With his extensive experience in sustainability and assurance, he represents Ernst & Young in various sustainability associations. Roger provides sustainability services including financial reports related to climate, CSR report advisory and assurance, international sustainability index, community investment, green finance, carbon pricing and strategy. Roger received his Ph.D. in Natural Resource and Environmental Management from National Taipei University and a Master of Accounting from Soochow University.

Comments (0)